Liquidity Performance Analysis: Yield Golfing — First Match Results

Overview

Yield golfing is a concentrated liquidity strategy comparative analysis campaign. Its goal is to measure the yield performance of ALMs over 2 weeks on the same grounds of strategy spreads, pairs, chains, and DEX. The competing ALMs use their methods of rebalancing and fee compounding to get the most out of users’ positions.

The First Match

The first match was held between A51 Finance and Gamma Strategies with the conditions mentioned below:

Campaign Timeline

- Start: 4 Sep 2024

- End: 19 Sep 2024

DEX: Uniswap V3

Pair: CRV-ETH

Fee Tier: 0.3%

Price Range:

- Min: 0.0000948 ETH per CRV

- Max: 0.0001287 ETH per CRV

Rebalancing Directions: Both sides

Fee Action: Compounding

Total Capital Per Strategy

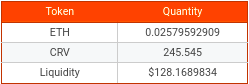

- A51 Finance: $128.17

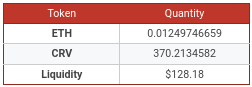

- Gamma Strategies: $128.18

Token Quantities in A51

- ETH — 0.02579592909

- CRV — 245.545

Token Quantities in Gamma

- ETH — 0.01249746659

- CRV — 370.213

Note: Due to the difference in the quantities of the two tokens, this won’t be an exact apple-to-apple comparison, but it’s still useful and fun to see how the two protocols compare.

How the Competitors Automate

In this section, we will try to understand how both ALMs automate the strategies and rebalance the asset:

A51 Finance (Trailing Rebalance)

A51 Finance has four types of range parameters that it takes into account for strategy rebalancing. The parameters are:

- Min Price: The minimum token0 per token1 price of the main range.

- Max Price: The maximum token0 per token1 price of the main range.

- Min Threshold Price: The minimum threshold price at which the rebalance should be triggered. This price is set behind the minimum price in the trailing strategy.

- Max Threshold Price: The maximum threshold price at which the rebalance should be triggered. This price is set above the maximum price in the trailing strategy.

This analysis uses the trailing rebalance mode while building the strategy. When the threshold price is hit, the contract takes the one-sided out-of-range liquidity amount and puts it right behind the updated price.

Gamma Strategies (Active Rebalance)

Gamma builds the pair ranges in two parts:

- Base Bounds: The main range around the price as Base upper and Base lower.

- Limit Bounds: The threshold bounds around the price inside the base range. When the limit bounds are hit, Gamma rebalances the strategy by swapping the asset that has been converted until the threshold price and keeps the range active through active swapping.

Gamma divides the deposit amount into two parts as well:

- Base Amount: The amount of liquidity spread across the base range.

- Limit Amount: The amount of liquidity spread across the limit range.

In Gamma, we had to use their pre-built strategy to deposit liquidity, so we matched the ranges in the A51 strategy to keep the experiment fair.

Note: An important aspect to know is that the token composition of both positions between Gamma and A51 was different based on the balance ratio difference.

Comparison Parameters

Following are the parameters that we used to identify the performance of the strategies:

- Liquidity vs. HODL Divergence (Divergence/Impermanent loss)

- Initial vs. Current Liquidity Divergence

Match Scorecard

A51 Strategy Liquidity Composition

A51 Finance Liquidity Progression from 4 Sept to 19 Sept:

A51 Strategy HODL vs Liquidity Chart

Gamma Strategy Liquidity Composition

Gamma Strategy Liquidity Progression from 4 Sept to 19 Sept

Gamma Strategy HODL vs Liquidity Chart

Performance Analysis

Before we dive into the analysis, it is important to know that this is an unbiased and fully neutral review of the strategies based on the market conditions and changes due to the rebalances and fees auto compounding. Having said that, let’s go straight into the analysis.

Looking at the market, we can see that the market initially saw the dip in ETH price from the start of the experiment going down from $2465 to as low as $2292 and then climbing back up to $2433. So in retrospect, we did a full circle of the price movement of the asset and the positions on both A51 and Gamma faced the divergence or impermanent loss.

For concentrated liquidity positions, this divergence in price plays the key role of capturing volume from trades, and side by side if the position is rebalanced or withdrawn during that time then it also results in the conversion of impermanent to permanent loss. So the race between the ALMs is about how graciously the strategies from ALMs tackle the divergence while earning concentrated fees from the trades.

Looking at the above data, we can see that the A51 strategy position came out positive in the divergence comparison with its initial HODL value and it beats the HODL by 5.37% when you account for the earned fees in it.

On the other hand, the story is the opposite of Gamma’s position as it stood short by -5.70% against its initial HODL value when you accounted for the earned fees along with the starting capital in it.

Link to stats sheet.

Conclusion

In the yield comparison between A51 Finance and Gamma Strategies, A51 achieved a 5.37% increase over its initial HODL value, benefiting from the concentrated liquidity strategy and earned fees.

In contrast, Gamma experienced a -5.70% decline from its initial value, despite the same market conditions and fee structure. This shows A51’s superior performance in mitigating impermanent loss while capturing more trading fees. A51 Finance emerged as the clear winner in this match.